The Good, the Bad, and the One Big Beautiful Bill – Part 3 of 3: Investor’s Guide

Introduction

A single piece of legislation hasn’t rattled so many real‑estate spreadsheets—and hijacked quite as many Slack threads—since the Tax Reform Act of 1986. The One Big Beautiful Bill Act (OBBB)—formally H.R. 1 of the 119th Congress—now detonates in a market already juggling 6 % mortgage coupons, sticky 3.8 % inflation, and a 5.5 million‑unit rental shortfall. Capital stacks are creaking, yet policymakers just lobbed a toolbox packed with both shiny incentives and razor‑edged caveats. Investors everywhere are pinning two Post‑it notes on their monitors: one titled Opportunity and the other Hazard—and wondering which will fill up first.

In Parts 1 and 2 of this series we walked through what OBBB means for buyers, sellers, and renters. Part 3 zooms the lens squarely on you—the asset hunter balancing cap‑rates, LIHTC algebra, sunset‑clause timing, and a surprise Visa Integrity Fee that could clip short‑term‑rental demand. Think of this guide as the factory service manual for Washington’s freshly minted wealth engine—complete with grease‑smudged diagrams, torque specs, and that bright‑yellow warning sticker Congress forgot to peel off.

So top up that oat‑milk latte, crack open a fresh Excel tab, and let’s calibrate which golden gears you can spin, which grinding cogs you’ll need to oil, and which flashing red lights ultimately mean step away from the deal.

The Good: Golden Gears for Investors

OBBB’s “good” column centers on deliberate levers that lower capital costs and widen the funnel for affordable‑housing deals. Think of these provisions as the polished brass gears inside a watch: small on their own yet able to multiply rotational force when linked together. Each incentive—larger LIHTC allocations, lighter bond requirements, an extended Opportunity‑Zone runway, and tax‑exempt rural interest—shrinks either the equity check or the borrowing cost, fattening spreads without exotic risk. Investors who move early can capture the boosted credits while competitors are still squinting at the bill’s more controversial headlines. The next sections break down the four sweetest gears and exactly how to engage them.

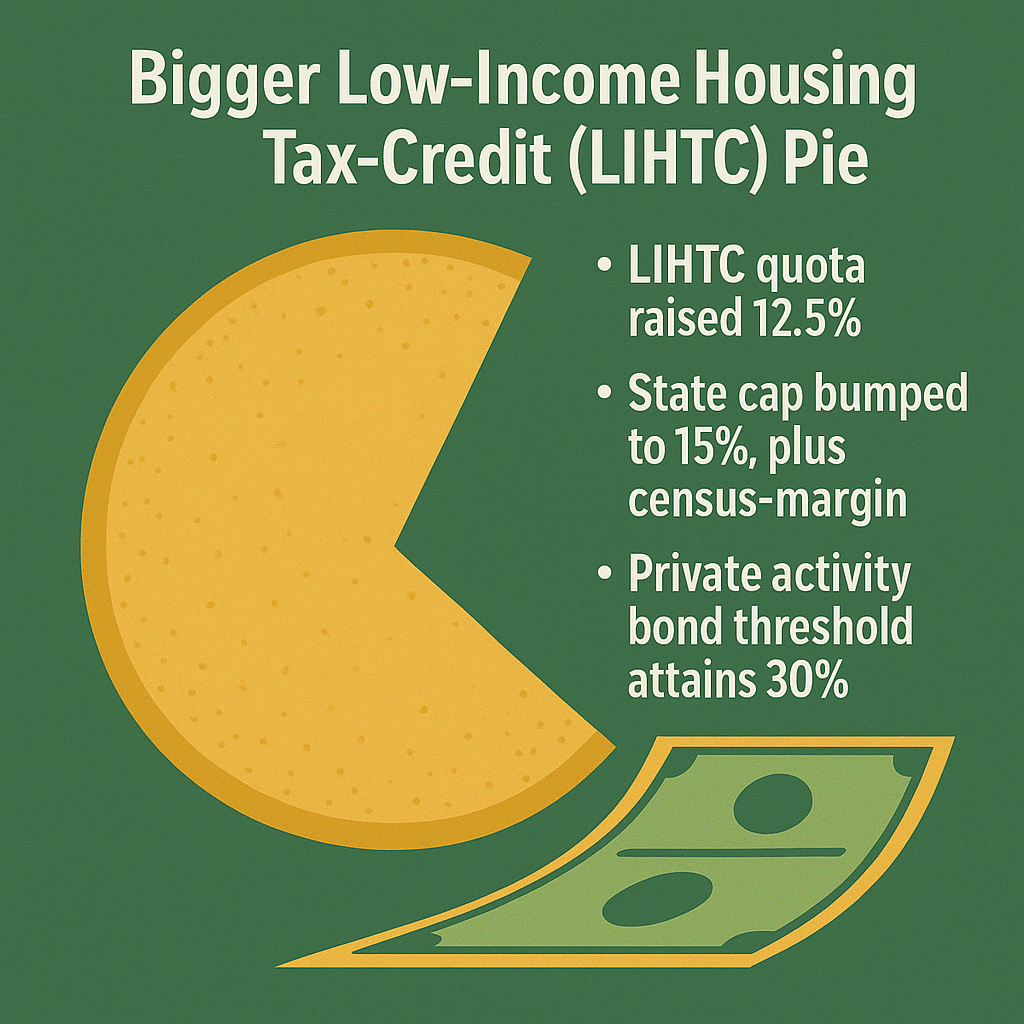

1. Bigger Low‑Income Housing Tax‑Credit (LIHTC) Pie

OBBB lifts the per‑capita 9 % LIHTC ceiling by 12.5 % for 2026‑2029 and drops the private‑activity‑bond requirement for 4 % deals from 50 % to 25 % ➜ more projects pencil and need less tax‑exempt debt (waysandmeans.house.gov).

2. Opportunity Zones—Round Two

The bill re‑authorizes and “enhances” Opportunity Zones through 2035, tightening census‑tract poverty thresholds (80 % ➜ 70 % AMI) while granting new reporting transparency (waysandmeans.house.gov). Early OZ funds returned 10‑12 % IRRs; extra runway could nudge exits upward.

3. Interest Exclusion on Rural & Ag Real‑Estate Loans

Section 111107 lets banks originate loans secured by rural property whose interest is federally tax‑exempt, mimicking muni‑bond treatment (waysandmeans.house.gov). Translation: lenders can shave 40‑60 bps and still meet spread targets—great news for farm‑adjacent STR cabins.

4. Small‑Manufacturer Expensing & Depreciation Boosts

The gross‑receipts threshold for small manufacturers jumps from $25 M ➜ $80 M, indexed thereafter, letting many builders use cash accounting and bonus depreciation (waysandmeans.house.gov).

- Bullet List 1 – Investor‑Friendly Provisions

+12.5 % LIHTC allocation (2026‑29).

4 % LIHTC bond threshold ➜ 25 %.

Opportunity Zones extended to 2035.

Rural‑loan interest becomes tax‑free.

These gears hum—if you file forms before Treasury’s forthcoming regs drop.

The Bad: Grinding Cogs & Hidden Costs

Even the shiniest machine has sand in the gears, and OBBB is no exception. Behind the headline incentives lurk line‑item levies and benefit claw‑backs that quietly erode pro‑forma margins if you’re not alert. The most talked‑about is the new $250 Visa Integrity Fee, but equally thorny are the 17 axed green‑energy credits, a one‑year Medicaid squeeze that threatens tenant stability, and the stubbornly frozen $10 k SALT cap. Each may look trivial in isolation; stacked together, they can shear a full percentage point off projected IRR—especially for leverage‑heavy sponsors. The next subsections dissect these grinding cogs so you can budget, hedge, or dodge them before closing.

1. Visa Integrity Fee ($250)

Starting FY 2026 nearly all B‑1/B‑2, F/M, H‑1B, and J applicants must pay an extra $250 refundable‑in‑theory surcharge (economictimes.indiatimes.com). STR hosts in World‑Cup cities fear diminished foreign bookings; USTA labels it a “self‑imposed tariff.”

2. Clean‑Energy Credit Guillotine

OBBB terminates or phases‑out 17 IRA‑era green credits—residential rooftop solar, heat‑pump rebates, clean‑vehicle credits, etc. (waysandmeans.house.gov). Investors eyeing eco‑retrofits lose up‑front tax shields, forcing deeper equity—or higher rents.

3. Medicaid & Nonprofit Clinic Cuts

A one‑year Medicaid funding ban for large abortion‑providing nonprofits could squeeze healthcare safety‑net budgets (timesunion.com). If clinics close, low‑income tenant stability may wobble—worth modeling in C‑class assets.

4. SALT Cap “Frozen,” Not Fixed

The Act keeps the $10 k SALT deduction limit through 2028, irking investors in high‑tax states (waysandmeans.house.gov).

- Bullet List 2 – Investor Headaches

$250 visa fee may dent tourist STR demand.

17 clean‑energy credits terminated or phased‑out.

Medicaid cuts raise tenant‑risk in subsidy‑heavy markets.

SALT cap freeze pinches high‑tax‑state buyers.

The Beautiful: A Long‑Game Wealth Engine

At first glance, OBBB’s “beautiful” column reads like a patience test, but the mechanics are deceptively powerful. When layered correctly, the expanded LIHTC basis and refreshed Opportunity Zone incentives act like dual turbo‑chargers—compressing equity needs and accelerating after‑tax yield. Add in the $60 billion municipal‑infrastructure carrot and you have city councils effectively subsidizing your entitlement timeline, often the costliest wildcard in development budgets. Because the enhanced allocations sunset while the assets themselves appreciate, investors who lock credits today forge a built‑in scarcity premium for tomorrow’s buyers. In short, the bill rewards thinkers in fifteen‑year cycles, turning political compromise into compounding cash flow.

1. LIHTC + OZ Stackability

Because LIHTC basis boosts overlap with revitalized Opportunity Zones, projects in poverty‑rate tracts under 70 % AMI may layer both credits—an equity waterfall dream (nelsonmullins.com, williamsmullen.com).

2. Sunset‑Timed Repricing

OBBB’s enhanced allocations expire 2029. History shows scarce credits inflate asset values post‑sunset (see 2017‑19 LIHTC pricing surge) (nlc.org). Buy during oversupply, ride scarcity later.

3. Municipal Push for Housing

National League of Cities notes OBBB sends $60 B to localities for infrastructure offsetting affordable housing mandates (nlc.org). Cities hungry for matching dollars may fast‑track rezoning for LIHTC/OZ combos.

Beauty Points

LIHTC + OZ dual qualification possible.

Credit‑supply drops in 2030 may lift valuations.

$60 B local grants grease zoning approvals.

Rural‑loan tax‑free interest yields cap‑rate compression.

Patience—as ever—is the secret fuel.

Strategy Blueprint

Phase I – Source & Underwrite

Use HUD and Treasury maps (updated Q1 2026) to overlay new OZ tracts onto existing LIHTC pipeline. Model 4 % credit deals at 25 % bond financing; sensitivity‑test tourist ADRs minus 8 % for visa‑fee drag.

Phase II – Capital Stack

Pair local bank rural‑interest‑exempt debt at <6 % with private equity targeting 8‑10 % pref. Offer state‑tax‑credit side letters in high‑tax jurisdictions to offset SALT cap sting.

Phase III – Build & Comply

File Form 8609B within 24 months; maintain Section 42 rent files. Budget MEP upgrades without federal solar ITC; investigate state‑level subsidies.

Phase IV – Operate Under New Norms

Raise ancillary revenue—covered parking, storage, pet rents—to blunt CPI‑linked limitations some states impose on OZ housing. Hedge STR units toward 30‑day corporate stays during World‑Cup visa‑fee window.

Phase V – Exit or Re‑Lever

Refi in 2030 once LIHTC allocation shrinks, compressing cap rates; or 1031 into rural‑opportunity‑zone mixed‑use.

Quick Action Steps

Download 2026 LIHTC/OZ overlay maps.

Stress‑test STR ADRs against visa‑fee scenario.

Lock rural‑interest‑exempt term sheet.

File Section 42 docs within Treasury’s 24‑month clock.

FAQs

Q: Will killing green credits crash retrofit ROI?

A: Not entirely; state incentives plus cheaper rural‑interest loans soften the blow (waysandmeans.house.gov).

Q: Does the visa fee affect Canadian tourists?

A: Yes—fee applies globally, indexed to inflation starting 2026 (economictimes.indiatimes.com).

Q: Can LIHTC allocations really run out?

A: Historically, states exhaust allocations within months; the 12.5 % bump is sizable but still finite (waysandmeans.house.gov).

Conclusion

OBBB’s blend of supersized housing credits, preferential rural‑lending treatment, and that surprising $250 immigration‑fee wrinkle forces investors to juggle carrots, sticks, and spinning gears simultaneously. Picture the statute as a Rube Goldberg contraption: gold‑coin credits tumble down a LIHTC chute, rural‑interest savings spin a flywheel, and a tiny visa‑fee marble tips a lever that could jostle short‑term‑rental projections off course. To make this machine spit out predictable cash instead of smoke, every cog must mesh before you pour the first yard of concrete.

Start by plotting your entire deal pipeline against the bill’s sunset schedule. The 12.5 % LIHTC boost fades after 2029, and the relaunched Opportunity‑Zone window closes in 2035. Acquisition, rehab, lease‑up, and refinance dates must march in lockstep with those expirations. Next, fold the rural‑interest exemption into lender term sheets; a 40‑basis‑point cut, amortized over 30 years, nudges a leveraged IRR from roughly 6 % to nearly 7 %. Don’t forget demand risk: model an 8 % decline in foreign‑visitor ADRs for any World‑Cup or Olympics host city hit by the visa fee, and stress‑test DSCR under that pressure.

Fortify your reserves. Park six months of PITI plus 5 % of hard costs in escrow so Treasury’s forthcoming Phase‑II rules—draft language is already circulating—can’t stall your Form 8609B. It may feel like overkill, but veterans remember the 2018 OZ reporting pause that iced dozens of projects for a quarter.

Finally, never navigate solo. I maintain live model libraries—cost‑seg templates, OZ waterfall builders, rural‑loan amortization sheets—and I’m happy to share them. Need help pressure‑testing your assumptions? Drop me a line at /contact or snag a 30‑minute strategy call. Day by day, brick by brick, we’ll calibrate Washington’s newest wealth machine until it hums, purrs, and prints greenbacks instead of headaches.